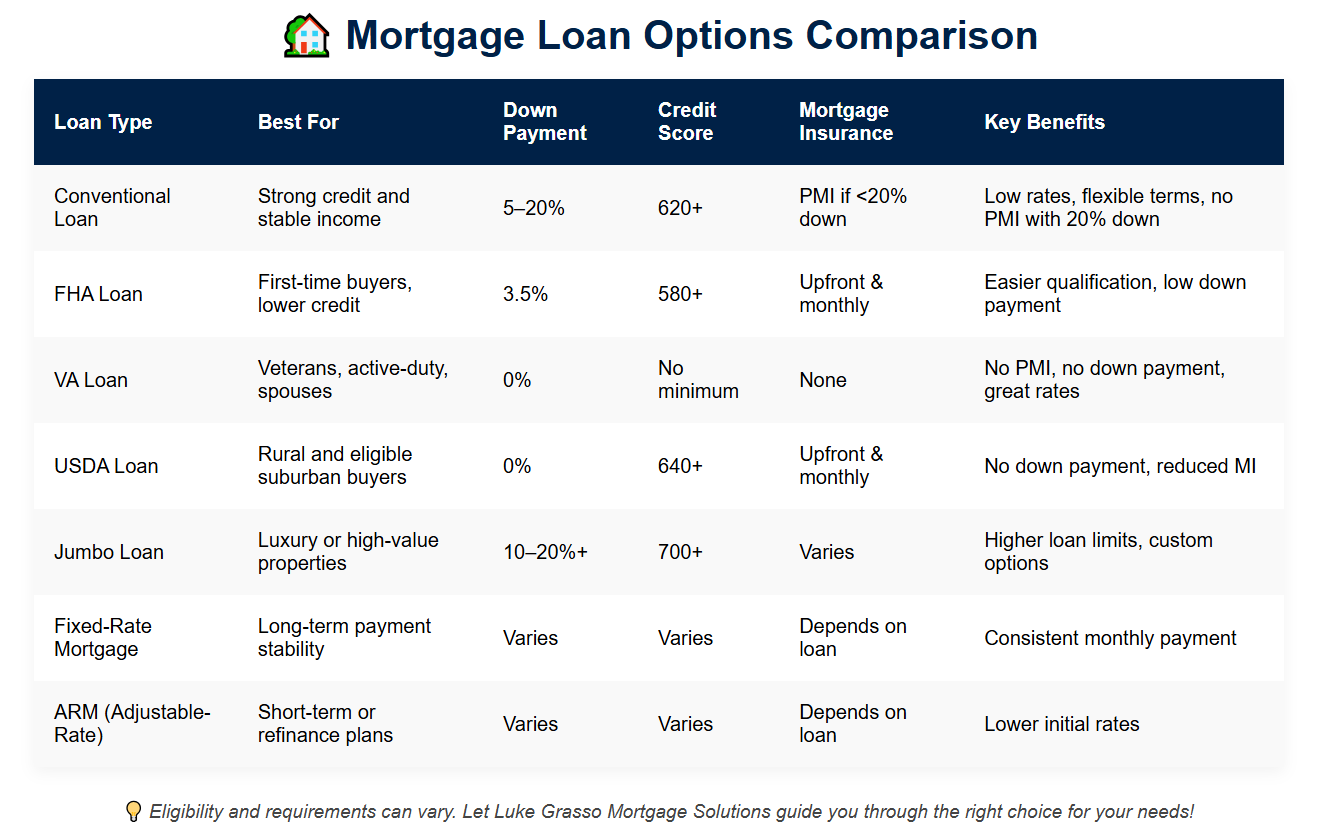

Description: The interest rate stays the same for the entire term of the loan (usually 15, 20, or 30 years).

Best For: Homebuyers who want predictable monthly payments and stability.

Pros: Stable payments; easier to budget.

Cons: Higher initial interest rates compared to ARMs.

2. Adjustable-Rate Mortgage (ARM)

Description: The interest rate is fixed for an initial period (e.g., 5, 7, or 10 years) and then adjusts periodically based on market conditions.

Best For: Borrowers who plan to sell or refinance before the adjustable period kicks in.

Pros: Lower initial rates.

Cons: Payments can increase after the initial fixed period.

3. Balloon Mortgage

Description: Short-term loan (5-7 years) with low monthly payments, but the full loan balance must be paid off in a large lump sum (the "balloon payment") at the end of the term.

Best For: Homebuyers who plan to sell or refinance before the balloon payment is due.

Pros: Lower initial payments.

Cons: Large lump-sum payment at the end of the term.

4. FHA Loan (Federal Housing Administration)

Description: A government-backed loan designed for first-time homebuyers and those with less-than-perfect credit. FHA loans require a lower down payment (as low as 3.5%).

Best For: First-time homebuyers or those with lower credit scores.

Pros: Low down payment; easier credit requirements.

Cons: Mortgage insurance premiums (MIP) are required.

5. VA Loan (Veterans Affairs)

Description: A government-backed loan for eligible veterans, active-duty service members, and their families. It often requires no down payment or private mortgage insurance (PMI).

Best For: Veterans and active military personnel.

Pros: No down payment; no PMI; competitive rates.

Cons: Only available to eligible veterans and service members.

6. USDA Loan (U.S. Department of Agriculture)

Description: A government-backed loan for low-to-moderate-income buyers in rural or suburban areas. It requires no down payment.

Best For: Homebuyers in rural or suburban areas who meet income requirements.

Pros: No down payment; low interest rates.

Cons: Location and income restrictions.

7. Jumbo Loan

Description: A loan that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA), typically used for high-priced homes.

Best For: Buyers looking to purchase high-cost properties.

Pros: Can finance expensive homes.

Cons: Stricter credit and income requirements; higher interest rates.

8. Interest-Only Loan

Description: The borrower pays only the interest for a set period (typically 5-10 years) and then begins to pay off the principal.

Best For: Borrowers who want lower initial payments and plan to refinance or sell before the principal payments begin.

Pros: Lower initial payments.

Cons: Payments increase significantly after the interest-only period; no equity is built during the interest-only phase.

9. Reverse Mortgage

Description: Available to homeowners aged 62 or older, allowing them to convert part of their home equity into cash. The loan is repaid when the homeowner moves, sells, or passes away.

Best For: Seniors who need extra income but want to stay in their home.

Pros: No monthly payments required; provides extra income.

Cons: Reduces home equity; fees can be high.

10. Conventional Loan

Description: A standard home loan not backed by the government. It typically requires a higher credit score and a larger down payment than FHA or VA loans.

Best For: Homebuyers with good credit and a stable income.

Pros: More flexible terms; can be used for any home type.

Cons: Higher credit score and down payment requirements.